By: DeFred G. FoltsIII Chief Investment Strategist & Eric Biegeleisen, CFA® Managing Director, Research

3EDGE is an active, tactical investment management firm, which means that we adjust our investment strategies when our outlook for the global capital markets changes. In contrast, a more traditional balanced portfolio is likely to remain fully invested in stocks and bonds regardless of the market environment. In addition, 3EDGE does not invest in individual stocks or bonds; instead, we create globally diversified portfolios through the use of Exchange Traded Funds (ETFs). Our stated investment objective is to generate attractive risk-adjusted returns on behalf of our clients by seeking to manage portfolio risk and smooth market volatility through a combination of our tactical approach and our broad portfolio diversification.

For most investors the pain of losing money in the stock market is far greater than the positive feelings from investment gains. The Nobel Prize-winning psychologist, Daniel Kahneman, called this the “loss aversion theory”1 and it helps explain why, during market corrections, investors may panic and make investment decisions that are simply not in their best long-term interest, i.e., selling low and buying high.

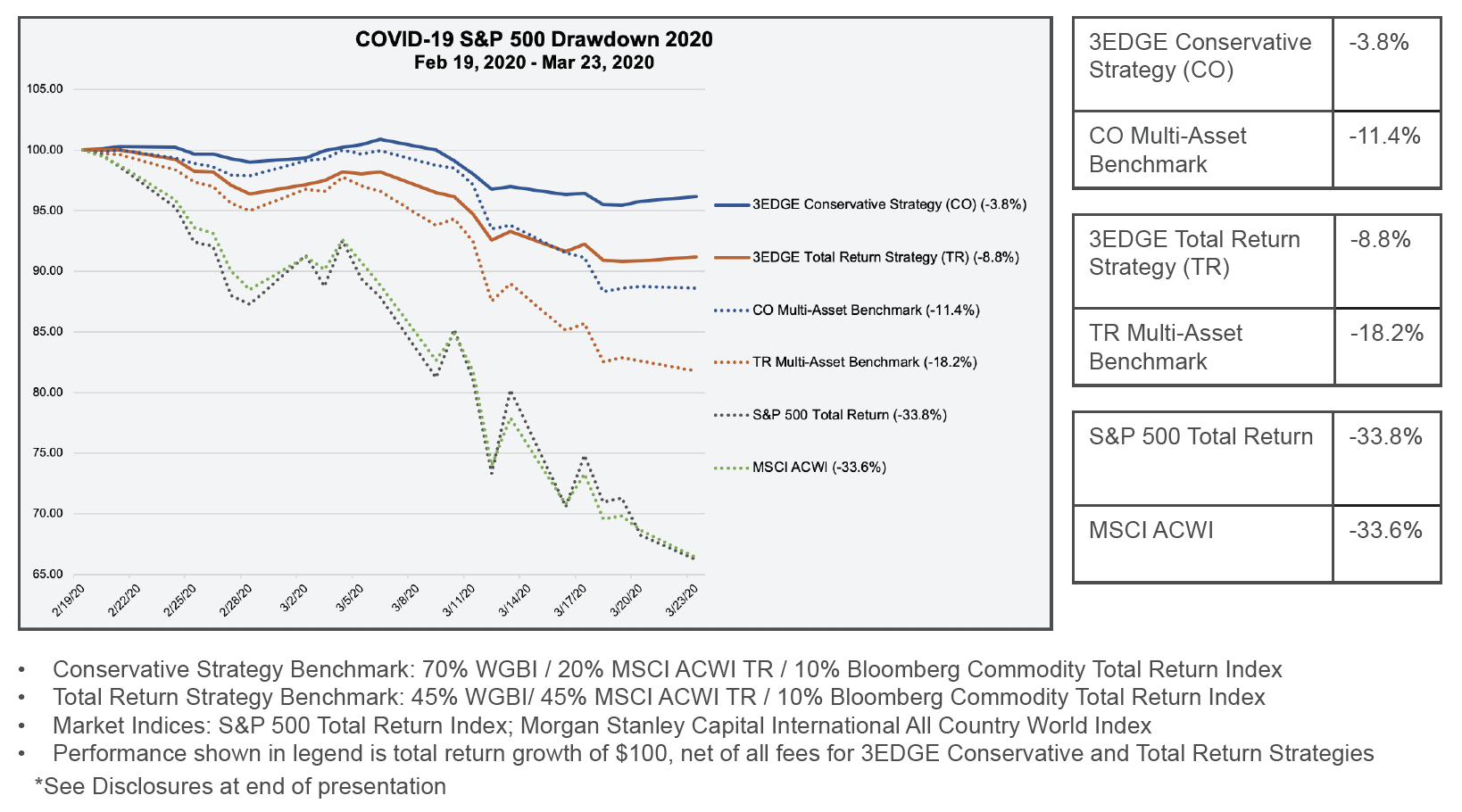

Figure 1 provides a recent example of how we utilize a combination of broad global asset diversification and a tactical portfolio management approach to manage risk.

In this example, based on our model research, we had reduced our overall equity exposure across our Strategies going into 2020 and increased our holdings in both gold and short-term U.S. Treasury securities. As a result, our Strategies held up as we would have expected during the sudden and sharp correction from mid-February through mid-March of this year.

Our approach to portfolio management also stems from our core belief that the global capital markets constitute a complex, nonlinear system of interrelated variables. This philosophy and approach are quite different from that of most traditional investment firms. For one, complex, non-linear systems do not lend themselves to analysis through the use of the Normal (Gaussian) distribution or a bell curve (see the blue line in Figure 2). A Normal distribution is the underpinning for traditional Modern Portfolio Theory but it underestimates risk in our estimation. We believe it is more appropriate to utilize a Power Law distribution to assess risk (see orange line in Figure 2) and understand the frequency and severity of price movements, both up and down.

A common characteristic of Power Law curves is that they can have fatter tails, as evidenced in Figure 2. The wider tails of the Power Law curve signify more data points with extreme values and a wider variation in the results. However, Modern Portfolio Theory, Value at Risk (VAR), and even the Black-Scholes option pricing model all rely on the Normal distribution or bell curve to assess risk. The problem with this approach is that in the real world the incidence of extreme market events (sometimes referred to as tail events) tends to be higher than projected by traditional risk models that rely on a Normal distribution or bell curve. Here are two recent real-world examples that demonstrate this problem:

From September 1, 2000, to September 30, 2002, the S&P 500 Total Return Index declined by nearly 45%. Assuming a normal distribution to measure risk, such a decline should occur approximately once every 38 years. In theory, that meant that investors shouldn’t have had to worry about another significant market decline for another 38 years. That’s not how things played out because, as we know, from November 1, 2007, to February 28, 2009, the S&P 500 Total Return Index declined by over 50%. Assuming a normal distribution, such a decline should occur approximately once every 201 years. And yet, these two material market declines occurred in the same decade!

These examples demonstrate how using traditional risk models that rely on a Normal distribution can be insufficient, particularly in attempting to understand tail risk -- those outlier adverse market events that can be so damaging to client portfolios.

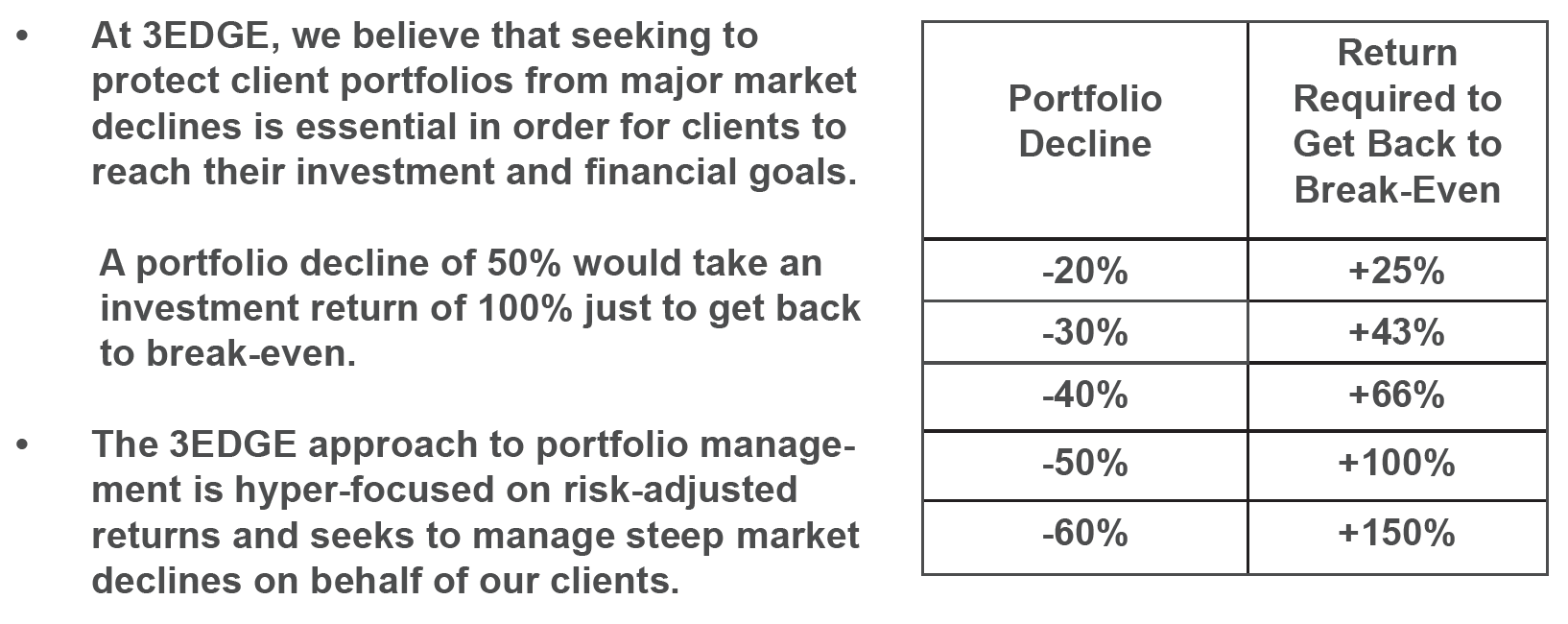

Figure 3 shows how the problem with underestimating the frequency and severity of extreme negative market events is compounded by math. As we know, a portfolio that declines by 50% requires a 100% return to get back to break-even (where you started), which is a big hole for an investor to have to dig out of. At 3EDGE, when analyzing potential investment risk, we also look beyond just measuring volatility or standard deviation and

focus on seeking to manage the potential maximum drawdown of a portfolio across the broadest number of potential scenarios, including extreme market events. Maximum drawdown represents the worst peak-to-trough decline that a portfolio may ever experience. To effectively manage portfolio risk, it is essential to go beyond volatility and bell curves (Normal distributions). This is why we believe our systems approach provides a more comprehensive understanding of investment risk.

Lastly, in our industry, we often hear the refrain that investors need to “hang in there” even through material market declines to avoid missing out on periods of major market upswings. However, that is very difficult for investors to do, particularly during periods of extreme market downturns. Nonetheless, we often see charts illustrating what would happen to the investment performance of a client’s portfolio if they were not invested during the ten best days or months of market performance over time. Not surprisingly, their investment performance would not be as good if they missed the best periods of stock market performance. However, there is an interesting corollary to this concept which gets back to our focus on risk management and seeking to avoid dramatic market declines. What if an investor was able to avoid the worst months of market performance? How would this impact their overall investment performance over the long term?

Figure 4 demonstrates that an investor would have been better served by avoiding the 12 worst months of investment performance (average annual return of +14.00%) than they would have been by “hanging in there,” and capturing all months, including the 12 best months, of S&P 500 performance (average annual return of 10.30%). The chart covers nearly 50 years of market history and therefore represents examples of both up and down markets.

Interestingly, the fourth row in Figure 4 shows that if an investor missed both the 12 best months of performance and avoided the 12 worst months, they would have still done better than the average annual return of the S&P 500 Total Return Index over the long- term, further illustrating the benefits of avoiding the worst periods of market performance.

All of the examples above point to how and why we look at investment risk differently from most traditional investment firms. To effectively manage portfolio risk, it is essential to go beyond bell curves and volatility (Normal distributions). We believe that our systems approach provides a more comprehensive understanding of investment risk. We seek to generate attractive risk-adjusted returns over full market cycles and believe that adding one or more of the 3EDGE strategies to a client’s overall investable assets could help manage risk and smooth market volatility while also seeking to be additive to investment returns.

DISCLOSURES: The opinions expressed by DeFred G. Folts III and Eric Biegeleisen of 3EDGE are provided for informational purposes only and are subject to change without notice. They are not intended to provide personal investment advice. Investors should only seek investment advice from their individual financial adviser. Observations include information from sources 3EDGE believes to be reliable, but the accuracy of such information cannot be guaranteed. Investments including ETFs, common stocks, fixed income and commodities involve the risk of loss that investors should be prepared to bear. Past performance may not be indicative of future results.

Performance for the 3EDGE Conservative Strategy and Total Return Strategy are shown net of actual management fees and all other expenses and includes the reinvestment of dividends and other earnings. The period 2/19/2020 – 3/23/2020 uses representative accounts for the respective strategies net of fees. These accounts were selected as they allow for weights and returns for the period noted and did not include non-3EDGE, client directed activity.

BENCHMARKS:

The benchmarks are rebalanced on a monthly basis and returns are gross of withholding taxes. 3EDGE Asset Management’s investment objective is to seek to earn attractive risk-adjusted returns over full market cycles. We do not actively seek to outperform any specific benchmark index on a relative basis. Nonetheless, we have established the Multi-Asset Benchmarks (“the Benchmarks”) for the Total Return and Conservative Strategies (“the Strategies”). The Strategies are not index funds and the portfolio holdings, country exposure, portfolio characteristics and performance will differ from that of the Benchmarks. The Benchmarks are simply a baseline against which we monitor the Strategies. They are intended to represent a passive, global, multi-asset class portfolio with similar risk characteristics to the Strategies. The Benchmarks have not been selected as a specific benchmark to compare to the performance of the respective Strategy but have been provided to allow for comparison of the performance of the Strategy to that of well-known and widely recognized indices. The Indices used in the Benchmarks are represented by total return prices. Indexes are unmanaged and therefore do not include fees and expenses typically associated with investments in managed accounts. One cannot invest directly in an index. Benchmark Data Source: Bloomberg.

DEFINITIONS:

The Morgan Stanley Capital International All Country World Index (MSCI ACWI) TR is designed to provide a broad measure of equity market performance throughout the world. Maintained by Morgan Stanly Capital International, it captures large and mid-cap representation across 23 developed and 23 emerging market countries, covering approximately 85% of the global investable equity opportunity set.

The Financial Times Stock Exchange World Government Bond Index (WGBI) is a broad benchmark providing exposure to the global sovereign fixed income market. It measures the performance of fixed-rate, local currency, investment-grade sovereign bonds comprising sovereign debt from over 20 countries, denominated in a variety of currencies.

The Bloomberg Commodity Index (BCOM) is a broadly diversified commodity price index tracking prices of futures contracts on physical commodities on the commodity markets. The Bloomberg Commodity Index Total Return (BCOMTR) reflects the BCOM on a “total return” basis, combining the BCOM returns with the returns on cash collateral invested in 13 week U.S. Treasury Bills.

RISK STATISTICS:

Maximum Drawdown is a measure of risk that captures the worst cumulative peak-to-trough decline of an investment or portfolio from any month-end data point to any other month-end data point. It shows in % terms how much money an investment portfolio would have lost before returning to its break-even point.

Hard Assets: Essential Ingredients for Building Diversified Portfolios