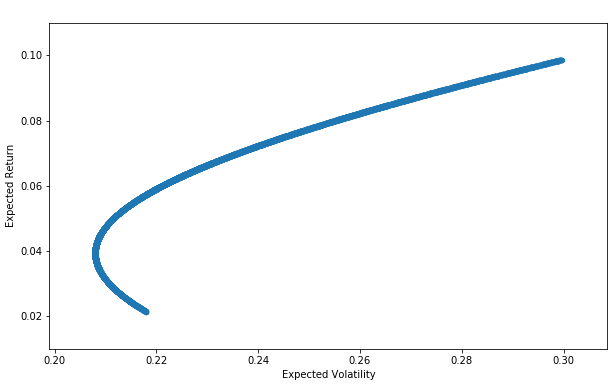

Conventional approaches only solve for Return and Volatility while assuming static correlations across time.

MODERN PORTFOLIO THEORY

Our model simultaneously solves across CAGR (Compound Annual Growth Rate), Sharpe Ratio (returns relative to volatility/risk), and Maximum Drawdown (potential maximum peak to trough loss) in aggregate for the combined asset classes that make up our investment universe which ultimately produce each portfolio strategy we manage for our clients.

3EDGE COMPREHENSIVE APPROACH

Output from our model research serves as our navigation system, informing our dynamic portfolio allocation decisions.